Xinyuan Real Estate (XIN) stock analysis

Overview

Xinyuan Real Estate is a Chinese real estate company listed in NYSE, which focuses on developing residential real estates in Chinese Tier II cities. These Tier II cities are larger and more developed with above average GDP and population growth rates. The company was founded in 1997 by Yong Zhang, who is still the company’s chairman and CEO. In 2007 the company committed an IPO to NYSE and became the first Chinese real estate company listed in NYSE. In 2012 they entered the US markets with three projects.

Financials

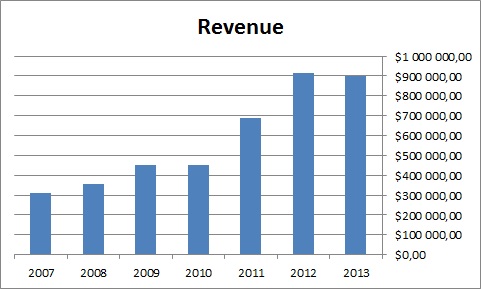

XIN has had some great growth. The revenue has tripled from 2007 to 2012 and earnings have increased steadily as well. In 2013 they made $1.63 profit per share of which they paid $0.2 as dividends, which gives a payout ratio of 12 %, which leaves a lot of room for growth. The company is still growing very fast so it makes sense to use the capital to growth rather than paying it as dividends. They paid their first dividends in 2011 and it has increased every year after that. This short time-scale doesn’t tell anything about company’s dividend policy, but at least according to Mr. Zhang they are committed to paying dividends:

“Finally, we are pleased with the continuation of our dividend program, announcing our fourth quarter dividend. We remain committed to this program as we progress through 2014,” concluded Mr. Zhang.

Risks

XIN definitely has some risks. There are a lot of examples of frauds committed by Chinese companies. Early this year the auditor of XIN, Ernst & Young Hua Ming, was suspended along with other auditors by the SEC, because they did not comply with SEC investigations of Chinese companies. This means that XIN probably has to find a new auditor for this year. This didn’t hit only Chinese companies, but also General Motors and Yum! Brands Inc. have to find new auditors.

Also exchange rates pose a great threat, since all of XIN’s profits are denominated in Chinese currency Renminbi (RMB). In future the role of USD will increase when XIN starts to make profit in the US.

The geographical threat is also obvious. Any changes in Chinese housing markets or economy could have big effects on the performance of XIN.

Valuation

XIN currently trades at about $4.95. Last year the EPS was $1.63, which gives for today’s price a PE-ratio of 3. The P/B ratio for XIN is currently 0.36. Both of these ratios are insanely low and it seems that the worst case scenario is already in the price. The dividend offers a 4 % yield, which seems quite low comparing to the risks. However I believe the company has a huge potential and the valuation level is way too low. Of course there is a risk that investors will never value the stock to its correct value but I’m not concerned because I think company will reward the shareholders with dividends anyway. That’s why I wouldn’t worry about the somewhat low dividend yield, because the company is still growing and the dividend has a great growth potential as well.

Full disclosure: Long XIN